Extended Warranty Merchant Accounts: Insiders Guide.

Extended warranty companies provide consumers with extra protection for their purchases. This includes covering the potential repair or replacement beyond general manufacturers warranty received with the consumer appliances. For businesses that offer extended warranty services, it is important to have a reliable merchant account; however, sponsor bank and payment process consider extended warranty a high-risk industry. Only specialized payment processors catered to the requirements of extended warranty merchants. The team at Quadrapay has created this extensive guide which discusses in detail all factors related to extended warranty merchant account and how to choose one. We are confident that after reading this guide you will improve the chances of your account approval significantly. Let’s begin.

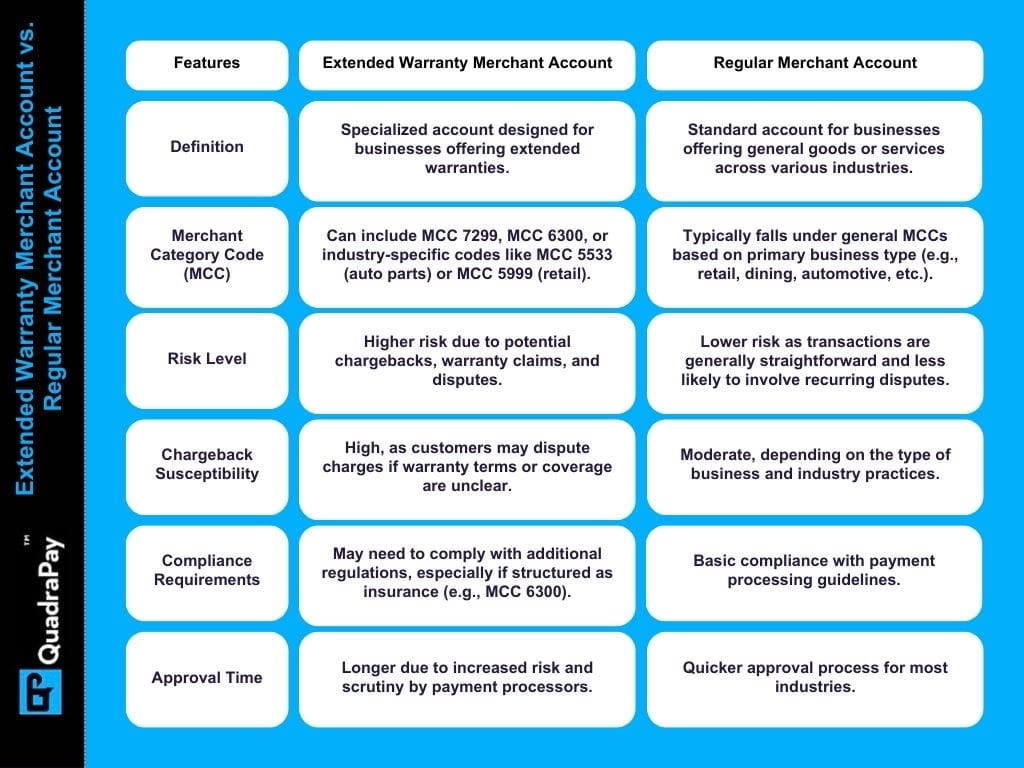

What is an Extended Warranty Merchant Account?

An extended warranty merchant account is a specialized type of merchant account that is made for businesses that sell additional warranty services and wish to accept credit and debit card payments for those sales. These accounts are provided by high-risk acquirers and sponsor banks as this industry faces high chargeback ratio, regulatory scrutiny, and also long-term financial liability.

Take payments with a reliable high-risk account

Rates and Fees for Extended Warranty Merchant Accounts

Now that you are aware that extended warranty businesses are termed as high-risk by banks and payment processors, it will not be a surprise for you that the rates and fees that you will be paying for accepting credit cards for your business will be slightly higher than a standard merchant account. Let us look at the breakdown of the rates and fees that you should expect with the merchant account.

The transaction fee that you pay for each transaction ranges between 3% to 6%. It basically depends on the risk profile of the merchant and the standard term sheet of the processor. If you are accepting cross-border transactions, then some payment processors may charge an additional 0.5% to 2% fee for international transactions to support your global customers.

In general, these accounts come with an upfront set of fees which can range from $500 to $1,000, and this is basically to cover the underwriting cost and also ensure that only serious enquiries are placed on the system. Having mentioned that, it is important to know that it is at the discretion of the payment processor if they want to waive the setup fees.

Payment processors don’t like chargebacks, and that is why to reduce the risk of chargebacks, payment processors charge a fee whenever a chargeback occurs. For extended warranty merchants, the chargeback fee ranges between $25 to $50.

Every high-risk merchant account requires a rolling reserve or a fixed reserve. In the case of extended warranty merchants, the rolling reserve is generally between 5% to 10%, and the money is held with the processor for a period of 3 to 6 months. This security deposit helps the processor against chargeback liabilities.

KYC (Know Your Customer) Requirements for Extended Warranty Merchant Accounts

It is mandatory for the payment processor to comply with the regulations and deeply evaluate the risk profile of the business. That is why the payment processor will ask the extended warranty merchant to provide a set of KYC documents. Let’s explore these documents in detail.

For business documents, the merchant needs to produce a business registration certificate. If it is an American business, then the merchant must produce an Employer Identification Number (EIN). If it is a European merchant, then a VAT certificate will be required. Along with these documents, the merchant also needs to produce articles of incorporation or similar partnership agreements, whichever is applicable.

For the financial document evaluation purpose, the merchant needs to produce 3 to 6 months of recent business bank statements showing consistent cash flow. In some cases, the payment processor may also ask for a profit and loss statement that helps the processor evaluate the financial health of the business.

The processing history helps the payment processor forecast the risk of potential chargebacks and also evaluate the sales projection of the merchant. The processing history should be recent (not older than three months) and should clearly display total volume, total chargebacks, total fees paid, and total returns.

The website plays a crucial role when it comes to the approval of extended warranty merchant accounts. It is important for the website to have clear terms and conditions, refund policy, and contact information listed prominently. A sample contract agreement for the customers should also be placed on the website.

To identify the business owners, the payment processor will require government-issued photo IDs. This can be a driver’s license or passport. Along with this, the business owner must also produce the latest utility bills for the company address as well as directors’ home addresses.

The underwriters’ compliance team will carefully review and validate these documents. Along with that, they will also check the website in detail. The processor may also run a credit check, and based on all these evaluations, the processor will come to a conclusion whether to approve the account or not.

Application Process for Extended Warranty Merchant Accounts

The application process for an extended warranty merchant account is pretty much similar to any regular merchant account. However, the only thing which differentiates this application process is the proactiveness of the merchant. There can be multiple instances where the processor will ask for additional documents and responses to certain questions. The proactive nature of the merchant to respond to such queries can significantly improve the chances of the account approval.

The application process starts with gathering all the KYC documents as listed above. The merchant should also ensure that the website is compliant with industry regulations and has clear terms and conditions, refund policy, and an active SSL certificate. You have to fill out a detailed application form which includes information about your business model, transaction volume, and average ticket size.

Once you are ready, you can send the application and the KYC documents to the payment processor for underwriting review. The total underwriting process for an extended warranty merchant account typically takes 1 to 2 weeks, and within this time frame, the payment processor evaluates all the documents, checks for chargeback history, financial stability, and regulatory compliance.

Based on the final decision of the underwriters, the payment processor will either reject the application or send you the approval. The approval is considered final after you sign a contract with the payment processor. Make sure you read the contract fully and, if need be, negotiate on the terms before signing the agreement. Once both parties sign the agreement, the payment processor shares the details of the Gateway login.

Integration Process for Extended Warranty Merchant Accounts

Once the account is active and you have received the login to the Gateway, it’s time for you to start the integration process. Some payment processors will have their own Gateway that you can integrate into the website; however, others will only provide you an integration sheet that will have details to be added to your existing payment gateway. Some of the finest payment gateways used by extended warranty merchants include Authorize.net and NMI.

If the processor is a full-stack solution provider, then you will get API keys, credentials, and complete documentation. The provider may also send you ready-to-use plugins that can be added to your website. These plugins are especially beneficial for merchants using E-commerce content management systems like Shopify, WooCommerce, Magento, WordPress, and more.

To complete the integration, follow the integration guide and start accepting test transactions. For this, the payment processor will give you test credit card details. Once the processor receives confirmation of test transactions, the gateway will be switched to live mode, and you will be able to accept real-time actual credit card transactions into your extended warranty merchant account.

FAQ Extended Warranty Credit Card Processing

What are some of the best Extended Warranty Providers in the U.S., U.K., and EU?

If you are considering using extended warranties for your home appliances or any other electronic equipment, then you must find a reputable provider. There are various service providers available in the North American and European markets. For example, Endurance Warranty is an excellent provider when it comes to getting comprehensive car warranty coverage in the US market. CARCHEX is another popular brand in the US market that offers vehicle protection plans. A few another name that you may wish to evaluate before making a decision is Allstate Protection Plans.

How can an extended warranty business reduce chargebacks?

There are various ways that can help reduce chargebacks, and the most important one is delivering excellent on-time services. In the extended warranty industry, the services are guaranteed for a longer period of time, and in case the customer requires the service and the service provider does not respond or does not provide good service, then it can raise the risk of disputes and chargebacks. Along with providing excellent service, it is also important to have clear communication with the customer. Make sure that your customer service team is available around the clock to listen to customers’ queries and should be fast enough to provide assistance and warranty to customers.

Is MCC 6300 suitable for extended warranties?

The actual merchant classification code which is more suitable for your business type will be decided by your payment processor. However, in general, when we talk about extended warranties, the product pretty much matches an insurance product for a specific time frame. Payment processors may ask extended warranty companies to provide an insurance license as these products resemble insurance policies because they cover repair and replacement risks. We suggest you contact your payment processor or a professional to confirm if your business is a perfect fit for MCC 6300, as it may require additional regulatory scrutiny.

Final Words by QuadraPay’s Extended Warranty Merchant Services Team

With the right extended warranty merchant account, your business can easily process credit cards, debit cards, gift cards, local payments, and international payments. By working with the right high-risk extended warranty credit card processor, you can be rest assured that your account will stay active for a long period of time without any complexities and stress. For more information about how Quadrapay can assist you in getting the approval of the right merchant account for extended warranty business, fill out the merchant account application on our website or you can also email us at info@quadrapay.com.

Recommended reading