Crowdfunding Merchant Accounts & Payment Gateways.

A crowdfunding payment gateway is a specialized bank account that allows crowdfunding platforms to collect payments from donors and investors. The gateway acts as a transaction processing platform between contributors and the campaign creators.

Crowdfunding platforms allow individuals to set up campaigns and collect contributions. Projects can be of various types, such as art, tech, games, films, and donation- or subscription-based crowdfunding. While these platforms make a significant impact in the lives of millions around the globe when it comes to credit card processing, they sometimes face serious challenges.

On the backend, crowdfunding platforms act as a marketplace for individuals who make accounts for causes. However, such platforms can bring in significant risk for payment processors. One fraudulent campaign can have a huge negative impact on the entire crowdfunding platform. This is one of the key reasons why most low-risk providers generally decline applications for crowdfunding merchant accounts.

However, it’s not a dead end for professionally managed and serious crowdfunding platforms. Specialized high-risk payment processors cater to the transaction processing needs of local and global crowdfunding websites and apps. Unfortunately, merchants may find it time-consuming to search for such providers. This is why the team at QuadraPay has written this extensive guide that explains most important factors related to crowdfunding credit card processing. We are confident that after reading this guide, you will be able to easily find a credit card processor for your crowdfunding project. Let’s begin.

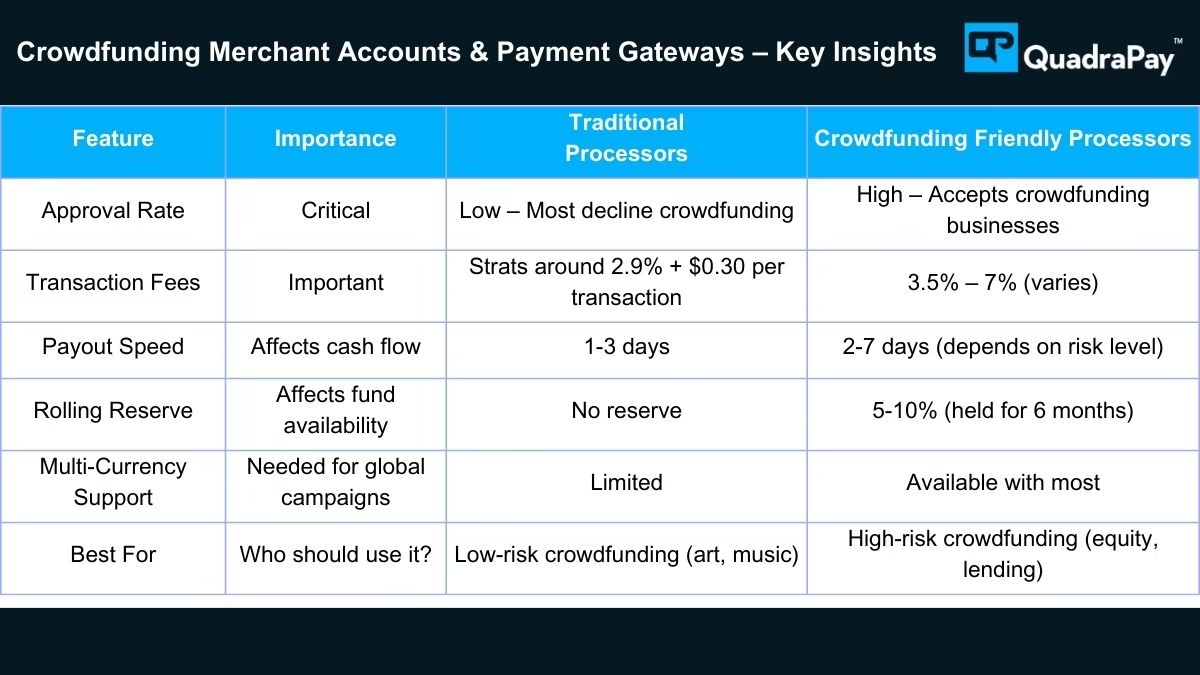

Crowdfunding Sites Need High-Risk Processors

According to SkyQuest Market Research, the global crowdfunding market size is expected to reach 7.82 billion US dollars with a CAGR of 16.7% by the year 2032. The projected growth rate is highly impressive. However, it is important to know that many payment processors consider onboarding crowdfunding merchants a big risk.

Crowdfunding differs from fundraising because in crowdfunding, the backer gets a commitment of receiving an exchange for their contribution. If the backer feels that they have not received the promised perk, then the backer may dispute the transaction and demand a refund. Such instances may lead to chargebacks.

Crowdfunding works on the basis of emotions and assurances. Some projects may not be fulfilled due to many reasons, such as mismanagement, production issues, or a new pandemic. These uncertainties also increase the risk of disputes and chargebacks from backers.

Other factors that make crowdfunding a challenging industry include inconsistent volumes, a high project failure rate, and a lack of collateral. All these factors make it difficult for crowdfunding merchants to obtain a credit card processing solution from traditional processors. However, high-risk merchant processors can definitely be in a better position to help.

Start your high-risk merchant journey now

How Crowdfunding Payment Processing Works

Crowdfunding payment processing involves many things beyond simply accepting credit card payments. Modern crowdfunding platforms must efficiently manage contributor onboarding, payment collection, compliance verification, fund safeguarding, payout distribution, and handling of refunds, all this while fully maintaining a secure and compliant environment for all the participants.

A typical crowdfunding payment flow starts when a contributor creates an account on the platform and supports a project by using his or her credit or debit card. Before accepting funds, crowdfunding platforms are sometimes required to verify the identity of the project creators, and in some jurisdictions, the contributors as well. This process is known as know-your-customer verification (KYC verification).

Once the contribution is received by the platform, then the funds are often held in a safeguard account or escrow-like structure until the campaign conditions are met fully. For example, some platforms release funds only after the funding goal is achieved. While many others allow project creators to receive the contributions immediately.

Once the campaign concludes, then the funds are distributed according to the platform’s payment model. The platform may deduct service charges, payment processing fees, and applicable taxes. This is done before releasing the remaining balance to the owner of the campaign. If a campaign fails to meet its objective, then the refunds may be issued to the contributors.

Because crowdfunding involves multiple parties, delayed fulfillment, and future delivery obligations, payment processors and acquiring banks are generally required to conduct enhanced risk management procedures. These procedures are meant to reduce the risk of fraud, chargeback, money laundering, and also regulatory exposure.

Crowdfunding Payment Flow

| Step | Description |

|---|---|

| Account Creation | Contributor creates an account on the platform. |

| Identity Verification | Know Your Customer (KYC) checks to verify identities and support regulatory compliance. |

| Payment Collection | Contributions are collected via credit card, debit card, bank transfer, or alternative payment methods. |

| Fund Safeguarding | Funds are held until campaign conditions or funding goals are met. |

| Campaign Monitoring | Transactions are checked for fraud, risk management, and compliance requirements. |

| Payout Distribution | Approved funds are released to the campaign owner after applicable fees and taxes. |

| Refund Processing | Refunds are issued when campaigns fail to meet requirements or contributors request eligible refunds. |

Types of Crowdfunding Payment Models

These days, crowdfunding platforms operate under several different business models, and each of these models present unique payment processing requirements and compliance obligations.

| Crowdfunding Model | Contributor Receives |

|---|---|

| Donation-Based | No financial reward |

| Reward-Based | Product or service |

| Equity-Based | Ownership stake in the company |

| Debt-Based | Loan repayment plus interest |

| Subscription-Based | Ongoing access, memberships, or recurring benefits |

Donation-Based Crowdfunding

A donation-based crowdfunding platform allows the supporters to contribute funds without expecting any financial return or physical reward. This type of model is commonly used for charities, churches, community projects, humanitarian causes, and personal fundraising campaigns.

Reward-Based Crowdfunding

Reward based crowdfunding allows contributors to receive products, memberships, services, or some kind of exclusive perks in exchange for their support to the project. This is one of the most common crowdfunding models used by startups and product creators in the U.S., Canada, and Europe.

Equity Crowdfunding

Equity crowdfunding enables large and even micro-investors to acquire ownership interest in startups or other private companies. Due to securities regulations, equity crowdfunding platforms are generally required to go through a very comprehensive compliance procedure and even detailed investor verification.

Debt-Based Crowdfunding

Debt crowdfunding, also known as peer-to-peer lending, is a model that allows contributors to lend money to borrowers and they do this in exchange for repayment plus interest. Payment processing requirements for such model often includes recurring payment collection, and investor reporting.

Subscription Crowdfunding

Subscription crowdfunding generates recurring support through weekly, monthly, or annual contributions. Membership communities, content creators, and nonprofit organizations are the type of entities that frequently use this crowdfunding model.

Website Requirements for a Crowdfunding Payment Gateway

To obtain a merchant account for crowdfunding, it is important that the website meets processor’s requirements. The website should be complete. An SSL certificate is mandatory. Additionally, the website must have terms and privacy policy pages. The customer care contact details should be in the footer section with logos of major card brands.

As your consultant, we say that sites that have good social media presence and natural organic traffic have better chances of getting approved. For this, we suggest startup crowdfunding merchants to work aggressively on the site and social media to generate traffic and a genuine user base. If the site has hardly any traffic, then how would underwriters trust that the site can do any business? Work on your site for easy approvals.

KYC Requirements for a Crowdfunding Payment Gateway

Providing all KYC documents to the payment processor at once helps improve the likelihood of getting approval. Here is a list of documents that are needed for a crowdfunding payment gateway.

Website WHOIS Certificate: This is to identify the ownership of the website. The domain must be in the name of the company, a major stakeholder, or the ultimate beneficiary of the company.

Business License: Certificate of incorporation.

Photo ID and address proof of directors: Payment processors require this information to identify the ultimate beneficiaries of the company. They will also run credit checks on the directors to assess their creditworthiness.

Utility Bill: This can be a telephone bill, internet bill, or any other bill that clearly shows the name of the business and the address.

Utility Bill of the Business Owners: Crowdfunding merchant account providers ask for this document to confirm the actual residence of the business owners.

Bank Statement: This statement helps the processor understand the financial strength based on the credits and debits.

Test User account: Some processors may ask for a test username and password for the website to ensure that it is being used solely for crowdfunding. They may also perform surprise audits. The login details are also asked for merchants in other industries such as online dating and matchmaking.

Common Payment Challenges for Crowdfunding Platforms

Operating a crowdfunding platform is not easy. It presents unique payment processing challenges when compared to traditional online e-commerce businesses. When you understand these challenges, then it can help you choose the right payment partner and also in reducing the operational risk.

Chargebacks and disputes.

Contributors may sometimes initiate chargebacks and they do this if they believe that a campaign has failed to deliver the promised reward. They sometimes also initiate chargebacks if the project timelines are delayed.

Fraudulent campaigns.

Payment processors carefully evaluate crowdfunding platforms and this is done because fraudulent campaign can damage consumer trust and also generate significant financial losses for the acquiring banks.

Regulatory compliances.

Depending on the jurisdiction of the crowdfunding platform, there may be certain requirements associated with KYC, AML, consumer protection and security regulations. It is important for the payment processor, the contributors and the crowdfunding platform owners to comply with such mandatory regulations and requirements.

Cross-border transactions.

Many crowdfunding campaigns attract international contributions. This creates a massive challenge which involves currency conversion, fraud prevention and international payment acceptance.

Payout management.

Crowdfunding platforms must accurately distribute funds among project creators while fully ensuring that they have proper accounting for platform fees, reserves and processing costs.

| Key Crowdfunding Payment Challenge | Recommended Solution |

|---|---|

| Chargebacks | Monitoring and dispute management |

| Fraud | Enhanced verification procedures |

| Compliance | Automated KYC and AML checks |

| International Payments | Multi-currency payment processing |

| Delayed Fulfillment | Proactive contributor communication and transparent project updates |

| Fund Distribution | Automated payout and settlement systems |

Key Features of a Crowdfunding Payment Gateway

Not every payment gateway is designed to support businesses in the crowdfunding industry. When you use a specialized crowdfunding payment gateway, then it provides you features that support compliance, scalability, and also contributors’ trust.

| Feature | Benefit |

|---|---|

| Merchant Account | Accept credit and debit card payments from contributors worldwide. |

| Payment Gateway | Secure payment authorization and transaction processing. |

| KYC Verification | Identity validation to support regulatory compliance and fraud prevention. |

| AML Monitoring | Protection against money laundering, fraud, and compliance violations. |

| Chargeback Prevention | Reduced financial losses and improved payment processing stability. |

| Multi-Currency Support | Accept contributions from international backers in multiple currencies. |

| Split Payments | Automatically allocate funds between the platform, project creators, and service providers. |

| Escrow Management | Securely safeguard contributor funds until campaign conditions are met. |

| Recurring Billing | Support subscription-based crowdfunding and recurring donations. |

| Reporting Tools | Improved financial visibility through transaction reporting and analytics. |

Why Crowdfunding Platforms Choose QuadraPay

It is a well-known fact that crowdfunding businesses, they all face unique payment processing challenges, and this requires specialized underwriting, risk management, and compliance expertise. At QuadraPay, we work with crowdfunding platforms worldwide. These includes operators in the UK, US, Canada, European Union, and Australia and we help them in obtaining reliable payment processing solutions through our acquiring partners.

| Advantage | Benefit |

|---|---|

| High-Risk Expertise | Better approval opportunities for crowdfunding and other high-risk businesses. |

| Global Processing | Accept payments from contributors and investors across multiple countries. |

| Multi-Currency Support | Expand your reach by accepting payments in various currencies worldwide. |

| Chargeback Management | Reduce dispute exposure with proactive chargeback monitoring and mitigation tools. |

| Dedicated Support | Receive personalized guidance from payment processing specialists. |

| Banking Network | Access specialized domestic and international banking partners. |

| Fast Approvals | Accelerated underwriting and onboarding processes to get your platform operational quickly. |

Whether you are launching a new crowdfunding platform or scaling an existing operation, QuadraPay can help identify payment solutions that support sustainable growth, improve payment acceptance rates, and provide the flexibility needed to operate in a competitive crowdfunding environment.

These solutions help the founders of crowdfunding platforms to meet their payment processing requirements efficiently. Our team truly understands the complexities that are associated with donation-based, reward-based, equity-based, and subscription crowdfunding models. We assist such merchants with payment gateway selection, underwriting preparation, international payment processing options, and also with chargeback mitigation strategies.

Whether you are just starting up and launching your brand new crowdfunding platform or you are trying to scale your existing operation, our team at QuadraPay can certainly help you to easily identify payment solutions that can support you for sustainable business growth.

Frequently Asked Questions About Crowdfunding Merchant Accounts

What is a crowdfunding merchant account?

A crowdfunding merchant account is a specialized payment processing solution that enables crowdfunding platforms to accept different kinds of payment methods, and these include credit cards, debit cards, and alternative payment methods. Crowdfunding platforms can accept payments from contributors while managing the risk associated with fundraising activities.

Why are crowdfunding businesses considered high risk?

Crowdfunding platforms are generally classified as high risk by acquiring banks, and this is because the campaigns may involve future product delivery, investor expectations, chargeback exposure, and increased regulatory scrutiny.

Can startups obtain a crowdfunding merchant account?

Yes, startups may qualify for crowdfunding merchant accounts. However, they must have a professional website, clear business model, proper documentation, and a very credible operational plan.

What payment methods can crowdfunding platforms accept?

Most of the crowdfunding platforms can accept well-known cards such as Visa, MasterCard, American Express, Discover. They can also accept alternative payment instruments such as ACH transfer, bank transfer, digital wallets, and cryptocurrency, depending upon the payment processor they choose.

What documents are required for approval?

The most common documents that are required for the approval of a crowdfunding payment gateway and merchant account includes the certificate of incorporation, government-issued photo IDs, proof of business and residential address, bank statement, website ownership verification, business plan, and processing history, if available.

What is KYC in crowdfunding?

Know Your Customer (KYC) is a procedure that helps in verifying the identities of the platform operators, campaign creators, and also sometimes the contributors. This helps in reducing fraud and to comply with various regulations.

What is AML compliance?

AML compliance is a set of rules that helps in monitoring transactions and user activity. It also helps in identifying suspicious behavior and preventing financial crime.

Can crowdfunding platforms accept international payments?

Yes, many crowdfunding platforms can now accept contributions from multiple countries, and this is done through international payment gateways and multi-currency merchant accounts.

How do crowdfunding payouts work?

The funds are generally collected from contributors and then they are processed through the payment gateway. After that, it is distributed to the campaign owners as per the platform’s funding model and the payment processor’s requirements.

What is an escrow account in crowdfunding?

An escrow or safeguard, safeguarded account temporarily holds contributors’ funds and this is only done until the predefined campaign conditions are satisfied fully. After that, the payouts are released.

How can crowdfunding platforms reduce chargebacks?

Crowdfunding and fundraising platforms can reduce the risk of chargebacks by ensuring transparent communication, verifying campaign creators, and providing clear refund policies. Some platforms also use various chargeback prevention tools.

How long does crowdfunding merchant account approval take?

The approval time can vary depending on various factors and by provider. However, generally, the approval timeline ranges between 24 hours to several business days. At Quadrapay, we have seen merchant accounts getting activated within 3 to 4 business days once all the documents have been submitted and the underwriting is complete.

Suggested Readings.

https://crowdfunding.wharton.upenn.edu/research/

https://funginstitute.berkeley.edu/wp-content/uploads/2013/11/Crowdfunding_Creative_Ideas.pdf

https://www.fca.org.uk/publication/thematic-reviews/crowdfunding-review.pdf