Weight Loss Merchant Accounts: Industry Guide

The global weight loss market has significantly expanded and is projected to reach a market size of $542.7 billion by 2033 (Source: Weight Loss Market, published Report Code: 36168). This growth is fueled by a range of products and services. However, banks have encountered challenges in processing payments for weight loss companies, leading to the need for specialized merchant accounts. Our team has extensive experience in helping businesses secure weight loss merchant accounts, which is why we’ve created this comprehensive guide to assist merchants in the weight loss industry in choosing a payment processor.

What is a Weight Loss Merchant Account?

A weight loss merchant account is a specialized type of credit card processing account designed to support businesses in the weight loss industry. This type of merchant account allows businesses to accept both e-commerce and retail transactions. Due to the nature of the industry, banks classify weight loss businesses as high-risk, making a specialized merchant account essential.

Merchant Category Codes (MCCs) in the Weight Loss Industry

Every merchant is categorized with a Merchant Category Code (MCC). These are four-digit codes established by ISO 18245. These codes help financial institutions determine risk assessments and interchange rates for merchants. For businesses operating in the weight loss industry, there are several relevant MCCs. Let’s look at these in detail.

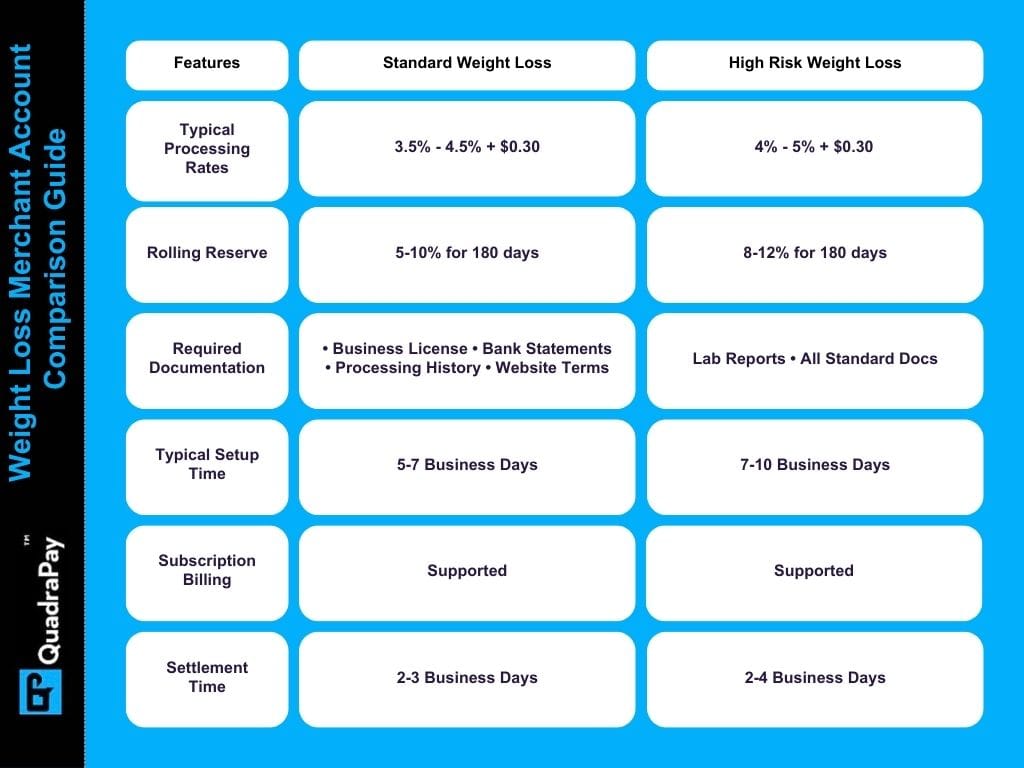

Weight Control Services (MCC 729934): This MCC is used for weight management businesses such as diet programs, weight loss centers, non-medical weight management, nutritional counseling, and weight loss coaching.

Physical Fitness Programs (MCC 729906): This MCC is for exercise-based weight loss services like gym-based programs, fitness centers, group training programs, exercise classes, and personal training facilities.

Fitness/Health Consultants (MCC 729901): This MCC is for professional services, including personal trainers, health coaches, nutrition advisors, wellness consultants, and fitness instructors.

Usage of Weight Loss Merchant Accounts

Weight loss merchant accounts are used by a variety of businesses, each selling products or services related to weight loss. Let’s look at some of these businesses and how they use weight loss card processing accounts.

Traditional Weight Loss Programs

Businesses in this category offer services such as exercise programs, nutrition counseling, and personal training. These programs typically involve customized exercise plans, diet charts, and consultations. Most companies accept credit card payments via websites and apps, often through monthly subscriptions.

Supplement Categories

Nutraceutical and supplement companies create products to help individuals lose weight. These include dietary supplements, nutrition products, and meal replacement programs, often sold through e-commerce platforms and sometimes via health clubs and gyms.

Medical Weight Loss

Medical innovations help people manage diabetes and body weight through medications, prescription weight loss drugs, telemedicine, and clinical programs. These providers often require payment solutions compatible with telemedicine, insurance, and EHR platforms. Due to medication involvement, additional compliance may be required.

Why Weight Loss Merchant Accounts High-Risk?

Sponsor banks and other card processing entities have been processing card payments for weight loss products for a long time. However, the overall experience has not been favorable. It is challenging to process payments for weight loss companies these days, as many factors make low-risk processors unsuitable for this industry. Let’s examine some of these challenges in detail.

High Disputes

It is well-known that effective weight loss cannot be achieved by taking a single initiative, such as consuming weight loss pills, wearing a weight loss belt, or signing up for an app subscription. Successful weight loss requires a comprehensive approach, including exercise, diet, sleep cycles, and various other factors. A significant portion of customers may struggle to lose weight, leading some to request refunds or initiate chargeback disputes. Some merchants experience chargeback rates exceeding 2%, which is above the approved limits. Additionally, customers often dispute transactions based on results, claiming that the outcomes were not as advertised. All these factors contribute to higher rates of returns and chargebacks, prompting sponsor banks to exercise caution when onboarding such companies.

Regulatory Scrutiny

Weight loss products and services are subject to intense scrutiny from regulatory bodies, creating a complex situation for underwriters. Many payment service providers (PSPs) find underwriting weight loss products so complicated that they often decline all applications from this industry. Underwriters must ensure that merchants comply with various regulations from agencies such as the FDA, the Dietary Supplement Health and Education Act (DSHEA), HIPAA, Good Manufacturing Practice (GMP) regulations, and facility registration mandates.

Financial Risks

The vast majority of weight loss companies rely on subscription models, but many processors are hesitant to handle recurring transactions, especially those starting with a free trial offer. This billing model can lead to revenue fluctuations, resulting in unstable income for processors. PSP’s prefer to work with merchants that can generate consistent processing volume, as this directly boosts the financial stability of the processing company.

Connect with a global network of high-risk payment experts

KYC Requirements for Merchant Account Approval

In order to approve a weight loss merchant account, it is crucial for the business to provide various documents to the payment processor for detailed review. The payment processor requires these documents to ensure that the merchant is legitimate and can be onboarded in accordance with underwriting policies. Let’s take a look at some of the mandatory KYC documents that need to be submitted to the merchant processor for review.

Valid Business Registration

A valid business registration document is essential to ensure that the merchant is legally registered and operating in accordance with laws related to health and wellness businesses. It is important to provide these documents in their latest version. A set of business registration documents may include the business registration certificate, tax identification number, EIN, and VAT number. Depending on the country of business registration, the required documents may vary. These documents demonstrate the business’s legal status and help build trust with consumers and financial institutions.

3-6 Months Processing History

For merchants who are just starting up, providing three to six months of processing history may not be possible; in such cases, merchants can provide business bank statements. However, for those merchants already accepting credit and debit card payments, it is mandatory to provide processing history. It is important to understand that underwriters can easily identify whether the merchant has previously processed credit card payments. Hiding this information can work negatively for the merchant.

Therefore, merchants should proactively provide recent 3 to 6 months of credit card processing statements. This documentation helps underwriters assess the merchant’s potential sales volume, return ratio, and current fees. By carefully evaluating these details, underwriters may present a more favorable offer. A weight loss company that provides processing history at the time of application demonstrates that it is a well-established business.

Bank Statements

Underwriters require bank statements for two main purposes. The first reason is to verify the details and validity of the depository business bank account where payments will be sent by the payment processor.

The second reason is to assess the financial strength of the business. A business bank statement with minimal transactions indicates a weak company. On the other hand, if a company has a bank statement showing decent credit and debit activity, as well as available funds, it can be assumed that the company is in good financial condition and can better manage credit risk challenges. A company with strong financials can also be considered a perfect fit for investing in marketing efforts, which will result in more transactions for the credit card processor.

Compliance Certificates

In the weight loss industry, compliance certificates may be required depending on the products sold by the merchant, as they confirm adherence to relevant health and safety regulations. This documentation assures underwriters that the merchant follows ethical practices. These certificates help underwriters verify that the products are safe and accurately formulated, as well as marketed correctly. Providing compliance certificates not only protects the business but also enhances its reputation among consumers and business partners.

Website Security Validation

Website security is important for all types of merchants, including those in the weight loss industry. On a secure website, customers feel more confident processing transactions. Underwriters require merchants to ensure their websites are fully secure by utilizing updated SSL certificates. Secure websites help reduce the risk of data breaches and fraud, which is particularly important for businesses selling health-related products, as consumers are more likely to share sensitive personal information when they feel their data is secure.

Privacy Policy and Terms of Service

A clear privacy policy and comprehensive terms of service are mandatory for weight loss websites. These documents should explicitly define how customer data is collected, used, and protected. Underwriters require these documents to ensure that the merchant’s website complies with data protection laws such as GDPR and CCPA. The weight loss industry often faces skepticism; however, providing transparent communication about privacy policies helps build consumer confidence and reduces disputes.

Clear Subscription Terms:

Most weight loss companies prefer to sell subscription-based products, making it essential to provide detailed subscription terms to both customers and underwriters. Merchant processors prefer transparent agreements that clearly display the billing cycle, cancellation policies, and refund processes. Merchants should minimize ambiguity in these terms to reduce chargebacks and disputes. It is crucial for the merchant to ensure that customers fully understand the terms of the subscription purchase; uninformed customers may contest transactions due to unmet expectations.

LegitScript Certification fro Weight Loss merchants.:

Weight loss companies must obtain mandatory LegitScript certification. This certification verifies that the merchant adheres to strict regulations required for selling prescription medicines and dietary supplements. Underwriters value this certificate because it demonstrates the merchant’s professionalism and commitment to safety, which is critical in the weight loss industry, where rigorous regulatory scrutiny is enforced.

Application Process for Weight Loss Merchant Accounts

The application process for merchant accounts in the weight loss industry involves several steps, and having a basic understanding of these can help make the process smoother.

Step 1 is to research payment processors that specialize in working with high-risk industries, particularly those experienced with merchants selling weight loss products. Such providers are often referred to as high-risk credit card processors.

Once you have identified a few payment processors, it’s time to compare their transaction fees, chargeback policies, and support services. It’s essential to verify if the chosen provider genuinely understands the regulatory landscape surrounding weight loss products. Some shady providers may onboard merchants by charging heavy setup fees only to immediately shut down the account and blame the merchant, which is unprofessional and potentially dangerous as it may also lead to the merchant being placed on the MATCH (TMF) list.

The merchant will be required to submit Know Your Customer (KYC) documents to the provider. Be prepared to respond promptly to any additional queries or documentation requests from the provider. Underwriters will assess the merchant’s risk profile and may conduct a background check and credit report on the business and its owners to evaluate potential risk.

If the application is approved, the merchant will be required to sign an agreement. It’s wise to read these terms carefully before signing. Afterward, the merchant will receive a welcome email with login credentials and integration details for the account.

The processor should provide easy integration options for popular eCommerce platforms like Shopify and WooCommerce. Processors should also have a dedicated support team to assist the merchant through the integration process. Once integration is complete, the merchant should perform test transactions using test credit card numbers. Upon receiving the processor’s approval, the merchant can start accepting live transactions.