What is an Offshore Merchant Account? [Complete Guide 2025]

An offshore merchant account is a type of bank account established in a foreign country to process credit card payments. Offshore card processing accounts are generally used by high-risk businesses. With offshore accounts, merchants can accept credit card transactions in various international currencies.

Every day, hundreds of high-risk merchants face rejections from domestic credit card processors. The reasons can be many, such as poor credit scores, industry reputation, or high monthly volume expectation. These challenges should not permanently restrict merchants from accepting credit card payments. Offshore merchant accounts can be a lifesaver for such struggling but genuine businesses.

Unfortunately, finding the right offshore merchant account is not a simple task. Many offshore processors have their websites in foreign languages. This creates a language barrier for American merchants. It becomes tough for domestic merchants to find offshore payment service providers.

QuadarPay has been providing affordable offshore merchant accounts since 2016. We have created this cheat sheet for you. It delivers important insights related to offshore processing services. We have covered various aspects, such as the key benefits, the application process, KYC requirements, and related questions. By the end of this sheet, you’ll have a solid understanding of offshore merchant accounts. Let’s begin.

Offshore Merchant Account vs. Domestic Merchant Account: Key Differences

Choosing between an offshore merchant account and a domestic merchant account is not just a banking decision; it can be a strategic move for your company. The decision can have a direct impact on your ability to scale, manage risk, and reach the global audience.

While a domestic merchant account offers easy setup and low rates, an alternative offshore account is perfect for businesses that operate in high-risk verticals. Offshore accounts offer greater flexibility, higher approval rates, and access to multiple currencies.

For businesses operating in adult streaming, CBD, gaming, nutraceuticals, peptides, or the adult toy industry, such solutions can be perfect.

Offshore acquiring banks typically require more documentation, enforce strict compliance protocols, and may take longer to onboard merchants when compared to domestic processors.

It is important for merchants to understand both the options and stack them up together to check all features. The table below breaks down the key differences between Offshore merchant accounts and domestic merchant accounts.

Offshore Merchant Account vs Domestic Merchant Account [Comparison Table]

| Feature | Offshore | Domestic |

|---|---|---|

| Approval Rate | Higher for high-risk | Lower for high-risk |

| Supported Industries | Broader (e.g., adult, CBD, gaming) | More restricted |

| Currency Support | Multi-currency | Single/dual currency |

| Setup Time | 1–2 weeks | 3–5 days |

| KYC | More documents required | Simpler for low-risk |

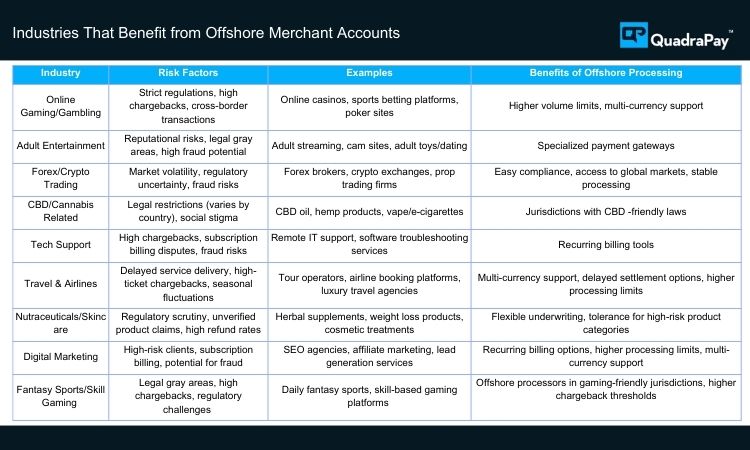

High-Risk Industries That Need Offshore Merchant Accounts

Offshore merchant accounts are important for high-risk merchants, as most domestic banks and payment service providers say no to them. Let us explore a few industries that depend on offshore credit card processors.

Online Gaming

The gaming industry is considered high risk as per sponsor banks. This concern is due to strict regulations, high chargebacks, and cross-border transactions. Domestic banks generally avoid working with gaming merchants. Offshore accounts are excellent options. This is mostly because offshore processors operate from jurisdictions that have relaxed gaming laws.

Adult Toys

Most banks avoid working with merchants from the adult toy industry due to reputational concerns. Such merchants need alternative payment channels. Merchants from sectors like adult streaming and dating can benefit from offshore processing.

Trading and Forex

Trading merchants like forex brokers and prop trading firms face uncertainties due to changing regulations and fraud risks. Offshore banks understand these complexities and provide excellent solutions to such merchants by taking calculated risks.

CBD-Related Products

Merchants that sell CBD-related products such as hemp, nicotine pouches, kava, kratom, vape, bong, and hookah struggle to get approval from domestic processors. Inconsistent regulations and social stigma make domestic processing difficult for these businesses. Many offshore banks operate in jurisdictions that welcome merchants from such industries.

Tech Support/Remote Support

Tech support companies face high chargebacks and returns. The industry is infamous for its high fraud ratio. All these factors make domestic providers extremely cautious about working with tech support merchants. This is why offshore merchant providers are best suited for these companies. These specialized processors can handle high-volume transactions for remote PC support merchants.

Travel & Airlines

The travel and airline booking industry is considered high risk because customers make payments for delayed delivery services. Such actions can result in excessive cancellations and can attract chargebacks. Many offshore processors specialize in supporting merchants from the travel industry. Some of the finest travel brands use international payment processors.

Supplements & Herbal

Nutraceuticals, supplements, herbal products, and vitamin businesses generally have a high refund rate. Along with that, such businesses operate in legal gray areas because of product claims and health concerns. Domestic banks generally do not prefer to work with such businesses because of complex regulations. Fortunately, offshore payment processors are more flexible when it comes to working with merchants from these industries.

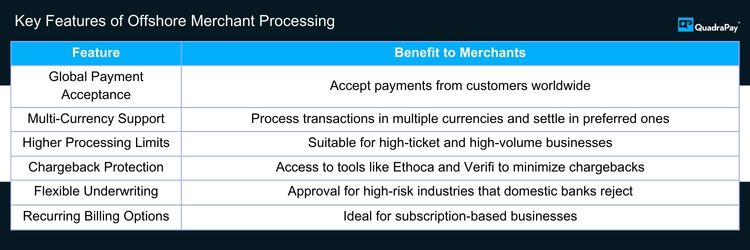

Key Features of Offshore Credit Card Processing

Offshore credit card processing offers various features. It is important to be aware of these features so you can efficiently use the account. Let’s explore these in detail.

Access to International Markets

Sometimes domestic acquiring banks limit a merchant’s ability to accept international card transactions. Many local processors only allow the acceptance of payments in the merchant’s home currency. Such an arrangement is a risk mitigation step, and it can be beneficial for the bank. However, it may result in financial loss for merchants. Offshore processors allow merchants to accept payments in various currencies and offer settlements in the merchant’s home currency.

Higher Processing Limits

Domestic payment service providers approve low monthly volume limits. They generally put a cap of USD 25,000. However, any e-commerce merchant that invests well in marketing can easily exceed this volume in just a few days. In such a scenario, business owners require alternative options to continue accepting payments. Offshore processing companies offer higher volume limits. Merchants that conduct high-ticket sales or have very high monthly sales volumes should explore such solutions.

Bad Credit Scores

Domestic providers require excellent credit scores for approval. It is a fact that every business faces challenges, and many are unable to maintain perfect credit scores throughout their operations. Businesses with poor credit scores face rejection from local banks. Offshore processors have relaxed credit score requirements.

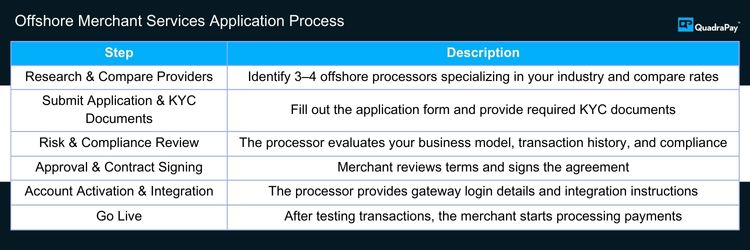

How to Apply for an Offshore Merchant Account [Step-by-Step]

The application process is simple. It begins with researching and selecting the right provider. Merchants should identify at least three offshore processors to compare. It helps in choosing the best offshore merchant account provider.

The next step is the application process. The merchant submits the application and KYC documents to the underwriters for evaluation. It is important to submit KYC documents without any manipulation.

The third step is the review. Underwriters at the sponsor bank check the merchant’s risk profile, financial stability, and compliance adherence. They may require additional documents. Whenever requested, the merchant should provide these documents promptly.

The last step is account approval. The provider sends an offer to the merchant. The merchant reviews the contract and then signs it. The approval timeline for an offshore merchant account is between 1 and 2 weeks.

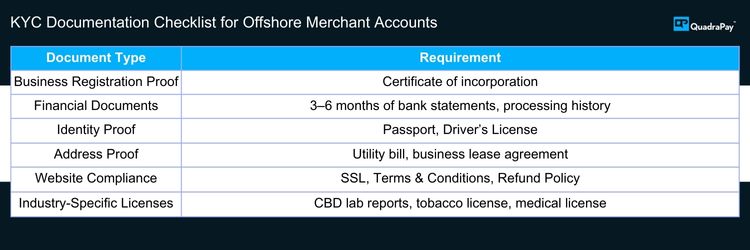

Offshore Merchant Account KYC Requirements

The KYC process is mandatory for every payment processor, irrespective of where they are located. The payment processor verifies the legitimacy of the applicant company by evaluating the KYC documents. Let us explore a few of these items in detail.

Business Registration Proof

The merchant must provide a copy of business registration. This can be a certificate of incorporation or any similar document. The documents should confirm that the merchant is registered and is eligible to conduct business activities.

Financial Documents

Merchants must provide 3 to 6 months of business bank statements.

Identity Proof

For this, merchants can provide government-issued photo IDs, such as a passport or driver’s license. Keep in mind that the ID proof must be valid and should be in English.

Address Proof

For proof of the company and the director’s address, the merchant can submit recent utility bills. It can be an electricity, phone, internet, or municipal bill.

Website Compliance

Merchants must ensure that the website has a shopping cart. The site should have pages for terms, refund policy, shipping policy, and privacy policy. The website must have detailed product information with pricing.

Certain industries are subject to high scrutiny. Mandatory high-risk registration may be applicable to certain MCCs. Your payment processor will inform you of this if it applies to your account.

Website disclaimers may be required for high-risk merchants. The website should clearly state the legal entity name on the checkout page. It should also display the billing descriptor and customer support details.

Industries like gaming, forex brokering, prop trading, and crypto exchanges etc require additional licenses. The processor will request lab certificates from merchants selling CBD or nutraceutical products. A tobacconist license may be required for any business selling cigars or tobacco products. For telemedicine practitioners, the underwriters may request a medical license and legit script certificate. A supplier agreement is necessary for dropshipping and e-commerce businesses.

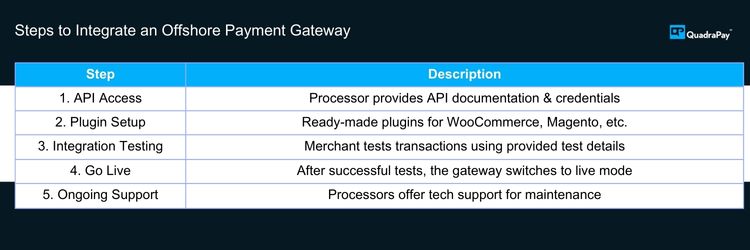

Offshore Payment Gateway Integration [API & Plugins]

After the approval, the payment processor will send the gateway access with an API integration guide. The payment processor may also provide ready-to-use plugins for shopping carts like WooCommerce, Magento, and OpenCart.

After integration, the merchant can perform some test transactions. The processor will switch the gateway to live mode after successful test transactions.

Future of Offshore Payment Processing & Global Merchant Services

Offshore merchant processors will continue to play a key role in the global e-commerce industry. While domestic processing companies are becoming very choosy about the industries they wish to support, offshore payment gateway companies are still open to merchants from various high-risk industries.

The stricter domestic processors become, the more demand for offshore processors will increase. However, it is important to remember that offshore credit card processors may not always be as flexible as they are today.

Offshore Merchant Account FAQs [2025 Edition]

Q1. How does an offshore merchant account work?

An offshore merchant account allows businesses to accept credit card payments through a bank or a payment processor which is located outside their home country. Transactions are settled through international wire and often with multi-currency support. This gives merchants access to a global customer base.

Q2. What is the difference between an offshore payment processor and a domestic one?

A domestic payment processor generally supports only local businesses and usually limits support for high-risk industries. However, if you look at offshore payment processors, they specialise in supporting high-risk businesses and they do provide multi-currency settlements. Sometimes, they also offer higher approval rates for industries such as Adult, Nutraceutical, CBD, and vapes.

Q3. Which is the best offshore merchant account provider in 2025?

The best offshore merchant account provider depends on the industry you operate in, your risk profile, and the target market. Top providers are those that offer transparent pricing, easy approvals, multi-currency support, and enhanced fraud protection. Quadrapay offers reliable offshore acquiring solutions that support high-risk industries globally.

Q4. Can I get an offshore merchant account with bad credit?

Yes, offshore payment processors are generally considered more flexible than domestic banks and they can approve accounts even if the business owner has a poor credit score. While additional documents may be required, most offshore processors prioritise the business model and processing history over the personal credit score of the UBO.

Q5. Do offshore merchant accounts support high-risk industries?

Absolutely. Offshore merchant accounts are best suited for high-risk industries such as online gaming, forex, adult entertainment, CBD, nutraceuticals, and tech support. As most of the domestic banks and payment processors often reject these merchants from these industries, offshore accounts work as an alternative payment solution for these struggling business owners.

Q6. What are the advantages of offshore credit card processing?

The first advantage of offshore credit card processing is the approval of the account. If a merchant keeps on struggling to get approval from a local or domestic payment processor, then approaching an offshore provider is the best option. They generally offer better approval rates for merchants from high-risk industries. They also support multi-currency transactions and offer higher processing volume limits. Such accounts allow merchants to expand globally without being limited because of local banking restrictions.

Q7. Is offshore payment processing legal?

Yes, offshore payment processing is completely legal as long as the merchant and the payment processors comply with the international regulations, local laws, and industry rules. You should choose a licensed and reputable offshore provider because this will ensure compliance and risk mitigation.

Q8. What documents are required for an offshore merchant account application?

The documents that are needed for offshore merchant accounts are pretty much the same as those that you would submit to a domestic solution provider. These generally include the business registration certificate, three to six months of bank statements, address proof, and photo IDs of the directors. The website should include terms and conditions, a refund policy, and a privacy policy. Additional documents may be required for industries and for merchants that operate in industries such as CBD, Forex, Nutraceuticals, and Airlines.

Q9. How long does it take to get approval for an offshore merchant account?

Approval time of an offshore merchant account can vary, but most of the time they are approved within 1-2 weeks after the KYC review. Some providers also claim instant approval, but the reality is that underwriting requires document verification to protect the bank and the merchant. This process requires time, so instant approval for offshore merchant accounts is not possible.

Q10. Can I accept multiple currencies with an offshore merchant account?

Yes, with Offshore Merchant Accounts, you can accept transactions in multiple international currencies. You may also request settlements in the currency of your choice.

Q11. What are the risks of using an offshore payment processor?

The most common risks include higher processing fees, strict compliance requirements, and potential delay in settlements if the chargebacks are excessive. When you work with a reliable provider, you can efficiently mitigate these risks.

Q12. Which countries are best for offshore merchant accounts?

The most popular jurisdictions for offshore merchant accounts include Cyprus, Hong Kong, Mauritius, and Seychelles. Belize used to be a popular location but now it is less favourable. The best choice for you will depend on your business type and target market.

Q13. Are offshore merchant accounts more expensive than domestic ones?

Yes, that is true. Offshore accounts generally come with higher transaction fees and may also involve a rolling reserve. However, the benefit is that they are more likely to approve the accounts.

Q14. Do offshore processors allow cryptocurrency payments?

Yes, the offshore payment processors support cryptocurrency payments. Bitcoin, Ethereum, and stablecoins alongside traditional credit card payments are supported.

Q15. Can small businesses or startups apply for an offshore merchant account?

Yes. Startups and small businesses can apply. However, the approval depends on the business model, compliance, and website readiness.

Q16. What is the cheapest offshore merchant account option?

The cheapest varies by industry and region. Providers in jurisdictions with lower taxes and relaxed regulations, such as Mauritius or Seychelles, often offer cost-effective solutions.

Q17. Do offshore processors support e-commerce businesses?

Yes, e-commerce businesses are among the top users of offshore merchant accounts.

Q18. What is the meaning of offshore payment processing?

Offshore payment processing refers to handling credit card transactions through a bank or processor that is located outside the merchant’s home country.

Q19. Do I need to register a company to get an offshore credit card processor?

Some countries require you to register a local company. Others allow foreign businesses without local registration. The requirement totally depends on the jurisdiction and acquiring bank.

Q20. How do offshore merchant account reviews help in choosing a provider?

Reviews can offer insights into approval times, fees, support quality, and reliability. They can help you avoid scams and select a trustworthy provider.