What Is a High-Risk Merchant Account in USA?

A high-risk merchant account is a specialized bank account that allows businesses operating in risky industries to accept credit card payments. Such industries have a larger exposure to credit risk, reputational risk, and regulatory complexities. This elevated risk exposure can be because of high chargebacks, regulatory scrutiny, or the sale of controversial products or services.

These specialized high-risk merchant accounts meet the unique card processing needs of those Industries that are generally declined by mainstream payment processors like Stripe and PayPal. With a high-risk merchant account, businesses can accept credit and debit card transactions. This can be done online as well as at retail stores.

High-risk merchant accounts generally come with strict contract terms, which means merchants have to pay slightly higher fees and must comply with additional regulatory as well as payment processor requirements. To reduce the credit risk, specialized high-risk processors use advanced fraud reduction tools like AVS, 3DS and CVV.

These accounts can be especially beneficial for businesses that operate on an international scale, sell high-ticket items, accept high-volume transactions, or accept recurring payments.

By using a high-risk merchant account, businesses that have been struggling to get approved by low-risk payment processors can continue the growth journey.

Such accounts allow merchants to accept payments through various methods such as cards, ach, bank transfer, and e-check.

Who Needs One and Why?

It is important to know that not every business needs a high-risk merchant account; these specialized solutions are built for businesses that are operating in industries like CBD, Vape, Adult entertainment, Collection agency, Property Management and Gaming. Businesses operating in these sectors have historically faced high chargebacks and elevated fraud risk.

Sometimes even a brand-new startup company without any transaction history can also be flagged as high risk just because of a lack of financial track record.

Any business that has frequent payment disputes from customers or offers services through a subscription model can benefit a lot from high-risk merchant accounts because these accounts have slightly higher risk tolerance.

A high-risk merchant account does not only offer you the ability to accept payments; it actually brings freedom to your business you will be able to grow and scale your business internationally and transact confidently without worrying about sudden account shutdowns or freezing of payments.

Key Differences: High-Risk vs. Low-Risk Merchant Accounts

Before you start searching for a payment service provider, it is important for you to know the key differences between high-risk and low-risk accounts. While both accounts allow merchants to accept credit card payments, their structure, pricing, and risk tolerance can vary significantly.

A low-risk merchant account generally has lower fees and has minimum onboarding requirements. Merchants get approved for a low-risk merchant account quickly. On the contrary, when you apply for a high-risk merchant account, the onboarding is done after extensive scrutiny, but it does offer more flexibility to unique business models or for those businesses that are operating in highly regulated Industries.

One of the biggest differences that you will notice is the risk appetite of the payment service provider. High-risk processors are able to support businesses that most low-risk processors always avoid. These specialized processors are able to do this by implementing various measures like advanced fraud mitigation tools, chargeback management systems, and adherence to extensive compliance standards.

High-risk merchant accounts are suitable for businesses operating in industries that are prone to volatility or are highly regulated. Such accounts allow merchants to accept high-ticket-value transactions, International payments and even complex recurring subscriptions.

| Criteria | Low-Risk Account | High-Risk Account |

|---|---|---|

| Onboarding Time | 1–2 business days with minimal documentation | 3–7 business days with enhanced due diligence and underwriting |

| Monthly Fees | Typically $0–$30, often waived by domestic processors | $10–$100+ depending on risk profile, vertical, and jurisdiction |

| Chargeback Threshold | Must stay below 1% to remain compliant with Visa and Mastercard rules | Also must remain below 1%; higher risk of scrutiny and MATCH list if exceeded |

| Accepted Industries | Traditional industries only (retail, professional services, SaaS) | Most verticals, including regulated and high-risk sectors like CBD, adult, forex, gaming, nutraceuticals, and travel |

| Risk Tolerance | Low tolerance; accounts can be terminated quickly for any red flags | High tolerance; designed for fluctuating chargebacks, compliance complexity, and larger volume risks |

| Reserve Requirement | Rarely required unless merchant history is weak | Frequently required. May include rolling, upfront, or capped reserves to mitigate risk |

Industries Commonly Flagged as High Risk

Certain industries are considered high risk by all payment processors. This can be because of the business model, product type, or consumer protection concerns. Most of the merchants operating in such industries face slightly higher than average chargeback rates, legal complexities, and inconsistent delivery of services.

Even if you operate a fully legal and ethical business, your industry alone can motivate the underwriters to flag your account as high risk. we have listed some of the most common high-risk industries, and we have also shared the possible reason for the classification.

| Industry | Reason for High-Risk Classification |

|---|---|

| CBD and Hemp | These are subject to evolving regulatory restrictions. The legality varies across countries and states and creates compliance risks for processors. |

| Adult Entertainment | Age-verification complexity, reputational risk, high refund rates, and legal liability related to explicit content. |

| Online Gaming | Frequently banned or restricted in multiple jurisdictions; linked to chargebacks from gaming addiction or regulatory intervention. |

| Travel & Tourism | Payments in these industries are often taken months in advance, making them vulnerable to cancellations, disputes, and fulfilment uncertainty. |

| Debt Collection | Handles sensitive consumer financial data, operates under strict legal frameworks like FDCPA/TCPA, and is prone to consumer complaints or litigation. |

| Tech Support | Remote service nature causes communication challenges, high dispute rates, and trust concerns especially with elderly clients. |

| Subscription Services | Recurring billing can trigger chargebacks due to unclear cancellation policies, renewal confusion, friendly fraud, or unrecognisable billing descriptors. |

| eCommerce Electronics | High average order value (AOV) combined with high fraud potential and increased risk of fulfilment claims or returns. |

| Forex & Crypto | Market volatility, speculative trading, frequent disputes, and heavy regulatory scrutiny. |

| Vape Products | Often subject to age restrictions, health warnings, and unclear legal categorisation. Many processors avoid due to potential liability and regulation. |

| Headshops | Sell items associated with tobacco. Considered high-risk due to perception, local laws, and reputational issues with banks. |

| Online Dating | Recurring billing, user complaints, adult-themed content, chargebacks over fake profiles, and difficulty in dispute resolution contribute to high-risk status. |

Just by being aware of the industries that are considered high risk by payment service providers and knowing the exact reasons behind these classifications, merchants can make adjustments and align their profile as per the expectations of the underwriters, and this can be done before they approach any payment service provider.

Why Businesses Are Classified as High Risk

Payment service providers evaluate each business’s risk based on their internal underwriting guidelines, card network rules, industry reputation, and transaction history. If a business exhibits characteristics that make it more prone to chargebacks, fraud, or non-compliance, it is often labeled as high risk.

Most of the times this classification does not mean the business is untrustworthy, it simply means the operating model involves more inherent uncertainty.

New startups with no previous processing history, merchants with poor credit scores, or those previously terminated by another payment service provider are also frequently flagged as high risk. Sometimes, merchants selling their products or services to international countries with inconsistent banking systems, operating without a physical address, or using a business model that involves delayed fulfillment (like travel or preorders), are seen as riskier by payment service providers and sponsor banks.

If you are a high-risk merchant, it is important to understand these classifications in detail. Knowing why you’re considered high risk will help you better prepare, present stronger documentation, set realistic expectations, and choose a provider that specializes in onboarding merchants like you.

| High-Risk Trigger | Explanation |

|---|---|

| No Processing History | Startups or new merchants with no established transaction history may be considered high-risk due to the absence of prior payment data. |

| High Refund or Chargeback Rate | If your monthly chargebacks exceed 1%, it raises red flags. Consistent refunds or disputes indicate customer dissatisfaction or fraud exposure. |

| Low Credit Score | Poor creditworthiness either personal or business can signal financial instability, increasing the risk to acquiring banks and processors. |

| Industry Regulatory Sensitivity | Operating in industries like firearms, CBD, dating, or debt relief invites extra scrutiny due to complex compliance requirements. |

| High Ticket Sizes or Monthly Volume | Processing large individual transactions or high monthly sales can increase potential liability in the event of fraud or chargebacks. |

| International or Cross-Border Processing | Dealing with multiple currencies, jurisdictions, or overseas buyers exposes merchants to currency volatility, tax complications, and increased fraud risk. |

The Application Process: Step-by-Step

When you apply for a high-risk merchant account, then keep in mind that it will require more in-depth due diligence when compared to a regular merchant account. You can get the approval of PayPal or Stripe within 24 to 48 hours, but for a high-risk merchant account, you may have to wait for 7 to 8 working days. This is because high-risk payment processes follow strict underwriting protocol, which involves carefully reviewing your business documents, checking your risk profile, your credit history, and many other factors. All this takes time.

The process starts with filling out the application form and submitting the KYC document. The underwriting team reviews all the information that you have submitted; it generally takes 3 to 7 business days. After the approval of the account, you will get the contract, which will have all the terms and conditions. This also includes pricing information. You should carefully review the contract and then sign it.

After signing the contract, you can start with the integration process, for which you will receive ready-made plugins as well as a detailed API document.

| Step | Details |

|---|---|

| Submit Application | Provide basic business details including contact information, ownership structure, business model, and projected monthly processing volume. |

| Upload Documents | Submit key documents such as government-issued ID, recent bank statements, utility bills, and processing history (if available). |

| Underwriting Review | Risk and compliance teams conduct KYC, AML checks, PCI compliance audits, and review of your website’s terms and refund policies. |

| Merchant Agreement Issued | You’ll receive a merchant agreement detailing transaction fees, contract length, reserve terms, rolling reserve (if applicable), and settlement timeframes. |

| Integration & Go-Live | After approval, you gain access to your payment gateway, reporting dashboard, and can begin processing payments within 24–72 hours. |

Documents Required for Approval

At QuadraPay, the KYC process is non-negotiable. When you apply for a high-risk merchant account with us, then our banking and acquiring partners perform a very comprehensive risk evaluation on your profile to check for exposure to chargebacks, complaint issues, previous fraud instances, and many other factors. The more complete your documentation is, the faster your approval can come.

The minimum document that you will have to provide to the underwriters for review will include the business licence registration, national ID of the directors and ultimate belly beneficiary owners, utility bill for the directors office as well as company address, domain registration group if you applying for E-Commerce merger account, bank statements, and any relevant other documents like lab certificate supplier agreement or industry specific licence

It is important for you to ensure that your website complies with the requirements of the payment industry. The website must include important pages like privacy policy, terms, refund policy, and shipping policy. Your contact information should be clearly visible in the footer section of every page of your website.

If you are a Startup and are considering getting approval of a high-risk merchant account, then you must provide a solid business plan, one that displays your revenue projection. proof of inventory and service readiness.

| Document Type | Purpose |

|---|---|

| Government ID (Passport, DL) | Used to confirm the identity of company directors. |

| Business License | Confirms that the business is legal within its jurisdiction. |

| Utility Bill or Proof of Address | Confirms the company’s physical existence. |

| Bank Statements (6 months) | Helps underwriters assess the financial health of the applicant company. |

| Processing Statements | Displays past transaction history and helps evaluate potential monthly volume, refund patterns, and chargeback ratios. |

| Website Review | Ensures the site has clear refund, privacy, and contact pages. |

| Business Plan (for startups) | Outlines revenue model, growth trajectory, and market positioning. |

| Refund Policy | Required for all eCommerce merchants. |

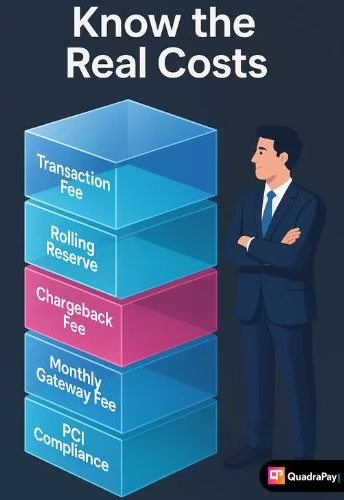

Fees, Reserves & Hidden Costs Explained

High-risk merchant accounts cost more when compared to standard ones. This difference is because of the greater risk exposure faced by payment service providers. The fees that a merchant pays for a high-risk credit card processing account include setup fees, rolling reserves, higher transaction percentages, and compliance charges. By understanding the fee structure, merchants can easily avoid surprises and negotiate in a smart way.

The transaction fee, commonly known as the merchant discount rate (MDR), ranges between 2.5% and 5%. Merchants also pay a monthly gateway fee. The processor will hold a percentage of each transaction for 3 to 6 months. It’s a strategic reserve that the processor can use in case the merchant gets chargebacks. The rolling reserve for our high-risk merchant account ranges between 5% and 10%.

The hidden costs that you should be aware of include the chargeback fee, which can range from $25 per incident to $50; early termination fees, which generally range between $200 and $600; and the penalty for breaching the monthly approved volume limit.

| Fee Type | Typical Range |

|---|---|

| Transaction Fee | 1.0% – 5% + interchange.. |

| Rolling Reserve | 5%–10% held for 90–180 days |

| Chargeback Fee | $25–$100 per dispute |

| Monthly Gateway Fee | $10–$30 |

| PCI Compliance Fee | $75–$125/year |

| Termination Fee | $250–$500 (if applicable) |

Top High-Risk Merchant Account Providers In USA

Choosing the right high-risk merchant account provider should be your priority because it will ensure fast approval, smooth cash flow, and proper regulatory compliance. This is especially important for businesses operating in industries like CBD, vaping, nutraceuticals, gaming, marketplaces, travel, and firearms.

The high-risk credit card processing landscape in the US is continuously evolving. Today merchants should work with processors that offer more than just MID (Merchant Identification Numbers). They should work with High Risk PSP that is stable and scalable.

Below is a comparison of some of the top-rated high-risk payment solution providers trusted across North America, Europe, and Australia. These include Durango, EMS, PaymentCloud, and QuadraPay. Each brings unique strengths for businesses with complex risk profiles.

| Provider | Specialisation | Why Merchants Choose Them |

|---|---|---|

| QuadraPay | CBD, adult, nutraceuticals, and more | Multiple partner providers in EU/US/AU/CA |

| Durango | Gaming, firearms, adult, regulated industries | Known for robust gateway compatibility |

| PaymentCloud | Subscription billing, tech support, nutraceuticals | Strong onboarding support, low monthly minimums, chargeback management tools, and Shopify/WooCommerce integrations. |

| EMS (Electronic Merchant Systems) | Retail, healthcare, B2C services, and recurring billing | Offers secure U.S. processing, ACH, fraud filtering, and quick onboarding with excellent customer service. |

Fraud Prevention & Chargeback Reduction Strategies

Fraud and chargebacks are the two main enemies of high-risk businesses. If left unmanaged, they can lead to account suspension and even MATCH listing. Fortunately, high-risk payment processors offer tools and best practices that help reduce exposure to disputes and fraudulent activities.

First, you should enable 3D Secure verification and CVV matching at checkout. These features create extra layers of customer verification. You should also use real-time transaction monitoring and velocity filters to block suspicious IP addresses or rapid-fire purchases.

Implementing chargeback alerts and notification services from well-known providers like Verifi and Ethoca is a smart strategy. These services notify merchants when a customer raises a complaint with their card issuer, giving you the opportunity to resolve it early.

Next, adopt dynamic billing descriptors to reduce customer confusion and clarify charges. Offer post-purchase SMS or email confirmations to customers, and send detailed invoices for their reference. On your website, include a flexible refund policy and proactively engage with customers before disputes escalate. This allows you to document refund-related communication and enhance overall customer satisfaction.

| Tool/Strategy | Impact on Fraud/Chargebacks |

|---|---|

| 3D Secure & CVV Checks | Authenticates cardholder identity and blocks unauthorised card use at checkout. |

| Verifi/Ethoca Alerts | Real-time chargeback alert systems that notify merchants before disputes are submitted—allowing refunds or resolution. |

| Dynamic Billing Descriptor | Displays a recognisable name on cardholder statements to reduce confusion and prevent “friendly fraud.” |

| Transaction Velocity Checks | Monitors purchase patterns and limits rapid, repeated transactions to detect bots or abuse attempts. |

| Chargeback Representment | Allows merchants to submit compelling evidence to fight and reverse illegitimate disputes. |

PCI-DSS, AML, and KYC are crucial compliances for high-risk merchants In US.

The actual foundation of a long-term, high-risk payment processing arrangement between a merchant and the payment processor is commitment to compliance. Regulations like PCI-DSS, KYC, and AML accomplish this. Sponsor banks and payment processors expect merchants to comply with all the regulatory guidelines.

Businesses accepting credit card payments on their website must have firewall policies, encryptions, and restricted access and should undergo recurring audits. this is all done to protect cardholder data in accordance with the PCI DSS standards. If such standards are not met by high-risk merchants, then the violation may result in penalties and account termination.

The KYC process ensures that government-issued photo IDS, business documents, and proof of Residence used by merchants are verified properly. it helps in preventing identity theft, fraud, and money laundering.

The anti-money laundering regulations are also extremely important when it comes to International transaction. They guarantee that the merchant is not unintentionally aiding financial crimes. Some complex Industries like crypto exchanges and money service businesses, all maintain their internal AML compliance documents. Such documents help merchants to present their profile in front of the underwriters in a professional manner.

How to Negotiate Better Terms & Lower Reserves

Many merchants think that the reserve percentage, transaction fees, or the reserve duration are absolutely nonnegotiable. However, in reality, that is not true, especially when it comes to high-risk processing. While most payment processors impose these measures to mitigate risk, they are willing to negotiate to adjust these terms if the merchant presents a strong business case.

For this, merchants should present a clean, low chargeback processing history. If your current refund rate is below 1% and you show 3 to 6 months of processing history with steady volume. Compliance readiness can also help you improve your chances of winning negotiations. If your website is PCI DSS certified, then it will signal low operation. Let the underwriters know about it.

If the payment processor does not accept your request for reducing the reserve percentage, then you can ask if they can support a tiered reserve structure. This way your processor can keep 10% for the first three months and then drop 5% thereafter. Some merchants also negotiate early release clauses, like if a chargeback stays under 0.5%, then the reserve can be returned faster. By having your paperwork ready and a seasoned negotiator like QuadraPay on your side, you can negotiate better.

| Negotiation Point | How to Approach It |

|---|---|

| Rolling Reserve % | Negotiate a staged release. For example: request 10% held for 90 days, reducing to 5% after consistent processing and low chargebacks. |

| Contract Length | Push for short-term contracts or trial periods with the option to renew based on processing history and performance. |

| Setup Fees | Request a waiver or discount on setup fees in exchange for volume commitment or a longer-term business relationship. |

| Transaction Fee Reductions | Offer realistic monthly volume projections or commit to a minimum processing volume to qualify for discounted rates. |

| Volume Caps | Negotiate a higher monthly cap review after 30–60 days of clean, stable transaction history without excessive refunds or chargebacks. |

Multi-MID, High-Risk Redundancy Strategies

In the high-risk world, you should adopt redundancy from day one. Remember, one fine sunny day, your sole PSP may suspend your account because of high volume, chargebacks, or industry bans. That is why building a Multi-MID (Multiple Merchant ID) strategy is essential.

By doing so, you distribute your processing volume across multiple processors. This can be done through domestic and offshore processors. You will be able to balance risk and ensure uninterrupted high-risk credit card payment processing.

Offshore accounts are particularly useful in this case for global businesses that have multiple entities. Such merchants generally operate in industries like CBD, adult content, or e-commerce. If you have companies registered in countries like the UK, Malta, Latvia, Lithuania, or Singapore, then you can easily get merchant accounts in those jurisdictions. These accounts will act as a backup merchant account for you.

Of course, this strategy is not straightforward. It requires setting up a company, office, and business bank account in another country. However, it’s definitely worth the effort. No entrepreneur ever wants to suddenly lose the ability to process credit card payments. No one wants to see frustrated customers who are unable to complete purchases due to card processing failures.

High-risk merchants can also implement redundancy by using alternative payment methods. Once you receive approval for your primary high-risk merchant account, proceed to reach out to other domestic providers. Keep adding alternative gateways like ACH, e-check, and crypto. This way, even if your one or two accounts get shut down, you can still accept payments. An experienced partner like QuadraPay can help you design a smooth redundancy plan.

| Redundancy Strategy | Purpose |

|---|---|

| Multi-MID Setup | Distributes transaction volume across multiple merchant IDs to prevent dependency on a single processor and reduce risk of sudden shutdowns. |

| Offshore Merchant Accounts | Enables cross-border flexibility, access to less restrictive banking jurisdictions, and freedom for industries limited by domestic regulations. |

| ACH/eCheck Backup | Provides a reliable alternative to card payments, especially useful for U.S. clients and high-ticket transactions that require lower fees. |

| Crypto Payment Gateways | Offers instant settlement, decentralised payment processing, and protection against traditional banking restrictions. |

| Smart Volume Routing | Automatically redirects transactions across multiple MIDs to avoid breaching volume limits and maintain account health. |

Common Pitfalls to Avoid

Even with the right merchant account in place, many merchants fall into avoidable traps. The most common mistake is not disclosing your business model accurately. Payment service providers need to know exactly what you’re selling and how you’re operating. Hiding details may sometimes fast-track your initial approval, but it will almost certainly lead to account termination when audits or customer complaints occur.

Another major mistake is ignoring your chargeback ratio. Consistently exceeding a 1% threshold can place you on the MATCH list, effectively blacklisting you from most processors for five years. To prevent this, you should monitor disputes, issue quick refunds, and use a chargeback alert system.

Avoid putting all your sales through a single payment service provider. If your volume spikes or a policy change occurs, especially with mainstream providers you could suddenly lose access to your funds.

Lastly, do not overlook compliance. Not being PCI compliant, or failing to display refund or contact policies on your website, can result in your account being rejected or frozen.

| Pitfall | Impact | Prevention |

|---|---|---|

| Withholding Business Info | Leads to account shutdowns, unexpected reserves, or immediate termination. | Be fully transparent during onboarding, including ownership, product details, and billing practices. |

| Ignoring Chargeback Thresholds | Triggers MATCH listing, increased rolling reserves, and loss of processor access. | Use chargeback alerts (e.g., Verifi), proactive customer service, and strong policies. |

| Relying on One MID/Platform | Any sudden shutdown can halt all revenue flow instantly. | Implement redundancy with ACH, crypto, offshore accounts, and smart routing. |

| No Website Compliance | Results in rejected applications or merchant account freezes. | Ensure terms & conditions, refund policies, privacy notice, and contact page are visible and up-to-date. |

| Delayed Customer Service | Frustrated customers escalate to chargebacks and dispute filings. | Use real-time chat, email ticketing, or call support with response SLAs to resolve issues early. |

FAQ High-Risk Merchant Accounts

Why is my business considered high-risk?

There can be many reasons behind the categorization of your business as high risk by payment processes. These factors include high chargeback ratio, the industry type, transaction volume, target markets, credit score, previous account shutdowns, and the business history

What industries are classified as high-risk?

Industries that are generally categorized as high risk by sponsor banks include CBD, adult, online dating, gaming, Forex, and debt collection.

How is a high-risk merchant account different from a standard one?

The key differentiator is that with the high-risk merchant account, merchants pay high fees, have to accept rolling reserves, and the application goes through strict underwriting. The approval process also takes a bit longer when compared to standard accounts.

Who decides whether a business is high-risk or not?

Certain industries have been classified as high risk by card schemes. The payment processors and the acquiring bank also classify merchants based on their risk appetite, industry data, merchants history, and complexity of compliance.

Can a low-risk business become high-risk later?

Absolutely, if a low-risk merchant starts getting a lot of chargebacks and the industry goes through regulatory changes or the merchant shifts the business model, then a low-risk merchant can be categorized as high risk.

Application & Approval Process of High-Risk Merchant Account

What documents are required to apply for a high-risk merchant account?

You should expect to submit a business license, bank statement, photo IDs of the directors, previous processing history, and your website URL for the approval of a merchant account.

How long does the approval process for a high-risk merchant account take?

The approval process for high-risk merchant accounts generally takes between 2 and 7 business days, depending on the documentation provided and the risk profile of the merchant.

What can I do to improve my chances of getting approved?

To improve the chances of your account approval, you must ensure that you implement transparent business practices, prepare complete documentation and maintain a low chargeback ratio.

What factors are reviewed during underwriting?

Underwriters will review your business history, corporate documents, check the owners’ credit, and evaluate your website. They will also check the processing volume, KYC/AML compliance and chargeback ratio.

Can I get approved with poor credit?

Yes, merchants with bad credit scores can potentially get approved for a high-risk merchant account; however, they will have to accept high reserves and fees.

Can a startup apply?

Yes, start-up businesses that have faced rejection from the low-risk processors can apply for high-risk merchant accounts; however, most providers prefer businesses with prior processing history.

Can I apply as a sole proprietor?

You can definitely apply as a sole proprietor; however, your chances will greatly improve if you have an LLC. QuadraPay can help you set up an LLC easily.

What if I don’t have a business website yet?

In most cases, the underwriters will require a business website; however, certain businesses can get merchant accounts without it. Ideally, you should build one during the onboarding process.

Can I change ownership details later?

Yes, merchants can change the ownership and use the same credit card processing account; however, they must inform the payment processor to get prior approval. This will help avoid any downtime.

Fees, Reserves & Pricing For High-Risk Credit Card Processing

Are fees higher for high-risk merchant accounts?

Absolutely, the fees that you pay for a high-risk merchant account are slightly high because of the associated risk and the management cost.

What kind of fees should I expect?

The most common fees that you should expect includes monthly fee, transaction fee, chargeback fee, and sometimes a reserve amount.

Are there hidden fees?

If you work with a transparent payment service provider, then you can ask for a full fee disclosure in writing. This will help you avoid hidden charges.

Is there a rolling reserve? For how long?

Yes, with most of the high-risk merchant accounts, you will have to accept a rolling reserve. This is generally between 5% to 10%, which is held for 3 to 6 months. The reserve helps to protect the payment processor against chargebacks.

How is the reserve amount determined?

The reserve amount or the percentage is calculated on the basis of business risk profile, expected volume and previous history.

Can I negotiate a lower reserve?

Absolutely, you can try to negotiate for a lower risk reserve; however, to do that, you must have a strong processing history.

What happens if I exceed monthly volume?

You must ensure that you do not process over your approved monthly sales volume limit. If that happens some processors may flag or pause your account. If you are expect a spike in transaction, then you should inform the processor.

Can I get my reserve refunded early?

Yes, that is possible; however, the final decision will be of the processor. Merchants that show consistent processing and low disputes can potentially get their reserve refunded early.

What is the policy on high-ticket transactions?

High-ticket credit card transactions are allowed; however, you must disclose this upfront. The approval for high-ticket transactions requires additional scrutiny.

High Risk Payment Processing Technical Integration

What payment methods are supported?

You will be able to accept all types of payment methods, such as credit cards, debit cards, ACH, and crypto.

Can I accept recurring payments/subscriptions/memberships?

Yes, recurring payments for subscription businesses are allowed. It is an ideal payment mode for clubs and SaaS businesses. With recurring payment platform, merchants can effectively perform dunning management and use flexible billing cycles.

Is there a processing volume limit?

Your processing volume limit will depend upon the underwriter’s decision. This limit can be increased based on your risk ratio.

What are the settlement times?

The settlement time frame for high-risk credit card processing is typically 2 to 5 business days.

Can I integrate the gateway with my website or CRM?

The merchant account comes with a detailed API that can be easily integrated into CRM, billing software and website.

Is it compatible with mobile apps?

Yes, the gateway can be integrated into apps by using mobile API and SDK.

Do you offer hosted payment pages?

Yes hosted payment page solution is available. This is beneficial if you do not want to go through complex API integration. You will be able to accept fully compliant payments through the branded hosted payment page.

Is 3D Secure supported?

Yes, our gateway supports 3D secure processing, and it helps in reducing fraud and chargebacks.

Can I send invoices to customers?

Absolutely, you can send invoices to your customers by using the invoicing tool.

Can I change my billing descriptor?

Yes, you can change the billing descriptor. However, you will have to inform the underwriters for approval to avoid confusion.

What are the supported currencies?

Our high-risk payment gateway allows multi-currency transaction. Businesses can accept payments in US dollars, euros, GBP, CAD, and many other currencies. The currency conversion is handled on a real-time FX conversion basis.

High-Risk Processing Security & Compliance

Is PCI-DSS compliance required?

Yes, full compliance with PCI DSS is mandatory for all type of merchants that accept card payments including those operating in high-risk industries.

What fraud prevention tools are used?

Our acquiring partners use a variety of fraud prevention tools, such as 3D Secure, AVS, velocity filters, and IP monitoring.

How do I handle chargebacks?

If you get a chargeback, then you should respond quickly and provide full evidence through the dispute management portal.

Can you help reduce chargebacks?

Yes, we can definitely help you in reducing chargebacks. For this, you will have to use chargeback alert services.

What is KYC/AML compliance?

It is a mandatory process that every payment processor must follow. It helps in identifying and verifying the business as per the industry’s standards.

What if my chargeback ratio is too high?

If your chargeback ratio increases, then the payment processor may put a temporary pause on your account. In case of excessive chargeback, the account may be terminated, and it may also be placed on the MATCH or terminated list.

Can my account be terminated without notice?

In rare cases, the account can be terminated without notice. This usually happens if the merchant violates terms and exceeds the risk threshold. To reduce the risk of account termination, you must take initiative to resolve the chargebacks and disputes quickly.

What are the consequences of getting listed on the MATCH list?

The consequences of being listed on the MATCH database can be serious, and it may restrict you from opening any other account for years.

High -Risk Account Management & Monitoring

What customer support options are available?

Our solutions are powered by some of the finest payment processors, and they offer customer support through multiple channels, including email, live chat, and a ticket system.

Will I get a dedicated account manager?

Dedicated merchant accounts are generally offered to high-volume merchants.

Will I get access to analytics and reporting?

Within the merchant account dashboard you can access analytics and option to download reports.

Can I upgrade to a low-risk account?

Yes, you can upgrade to a low-risk account; however, for that, you will have to present a good processing history and minimum disputes.

Is auto-decline rule setup?

The gateway implements various risk reduction measures, such as declining transactions coming from risky locations or IP addresses or because of card mismatch, and more.

Can I add multiple MIDs in one dashboard?

Yes, by using a specialized payment gateway, you can add multiple merchant IDs in a single dashboard.

Does the merchant account support CBD/hemp businesses?

Yes, our payment solutions are available for CBD and hemp merchants in certain countries.

Do you support businesses in the adult niche?

Yes, we support adult-oriented businesses; however, they must comply with the mandatory regulations.

Can I migrate to your services?

Yes, as our services come to you at low cost, you can certainly migrate to our solutions. Our team will provide you full support in the migration process.

Choosing a High-Risk Processor

What should I look for in a high-risk payment provider?

You should look at how transparent the provider is and what experience that company has in onboarding merchants from high-risk industries. You should also check what kind of fraud reduction tools they have in place. Along with that, you should also check their reviews.

Why choose you over PayPal/Stripe/Square?

While PayPal, Stripe and Square may support some high-risk industries, when you work with us, the support is available to a larger list of high-risk verticals. Our core service is high-risk processing; you can get a dependable solution from us.

Do you have industry experience?

Yes, we are highly experienced in the high-risk credit card processing industry, and we have supported various CBD, gaming, adult, and debt collection merchants across multiple nations.

High-Risk Merchant Account Onboarding Process

Do you offer onboarding training?

Yes, once your account is activated, our team will assist with the integration and give you a walkthrough for the merchant dashboard.

Are sample contracts available?

Yes, we can share the contract with you before you sign the agreement. This will help you to understand the key terms and conditions involved.

How do you stay compliant with card regulations?

Our acquiring partners are some of the most reputed players in the market, and they fully comply with the card schemes’ guidelines, including those of Visa and MasterCard.